.jpg)

Interested in learning how to make a budget and take control of your finances? It's a great goal to set for yourself. The trick is figuring out which approach makes the most sense for you. There are so many tools and methods out there that many people simply don't know where to start.

Once you know how to make a budget that fits your life, you will be one step closer to true monetary security. With the right tools and strategy, you can identify where your money is going each month and make meaningful progress toward your financial goals.

This comprehensive guide breaks down the finer points of how to make a budget and provides practical tips to help you manage your money smarter.

What is a budget?

A budget is a financial plan that outlines how you'll use your money over a specific period of time. Most people learn how to make a budget that spans a month, as this is the most practical approach. Your budget will help you allocate money toward essential bills, savings, and personal spending while preventing you from stretching yourself too thin.

Budgeting allows you to be proactive with your money. Instead of waiting for an emergency to put you in a financial hole, you can save cash to cover any surprises that may pop up along the way.

Why budgeting is important

When you know how to make a budget, you can unlock benefits like:

- Less stress about bills

- Greater financial control

- Improved saving habits

- Better preparation for emergencies

- Clear progress toward your financial goals

Without a budget, all of those small daily expenses can eat away at your bank account. Before you know it, you may find yourself short on bill money or struggling to make payments on time. If you don't have enough savings to cover the difference, you could be forced to take on debt.

Learning how to make a budget ensures that your priorities align with your income. You can plan spending, including those small coffee trips, eating out, and entertainment, so you don't overdo it.

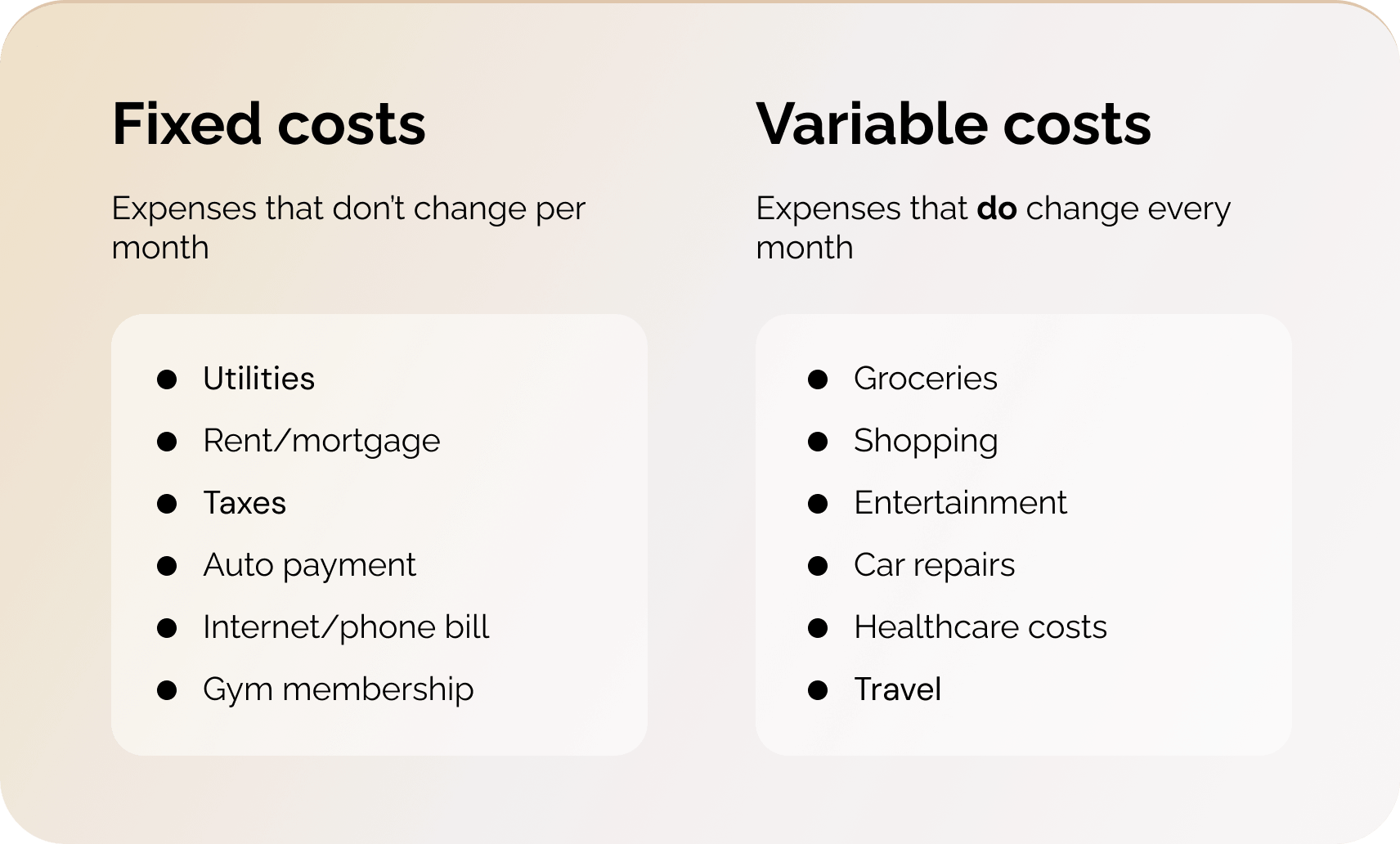

Fixed vs. variable expenses

Before learning the specifics of how to make a budget, it's a good idea to review some financial basics.

One of the biggest factors at play is fixed versus variable expenses. Your fixed expenses are the same each month. For example, your car payment and rent are fixed.

Variable expenses can include both essential and discretionary spending. For instance, your grocery and utility bills can fluctuate, but they're essentials. Entertainment is discretionary, but it also fluctuates.

When exploring how to make a budget, you should divide your expenses into fixed and variable categories. Grouping them in this way will help you understand where you have room to cut back or make adjustments.

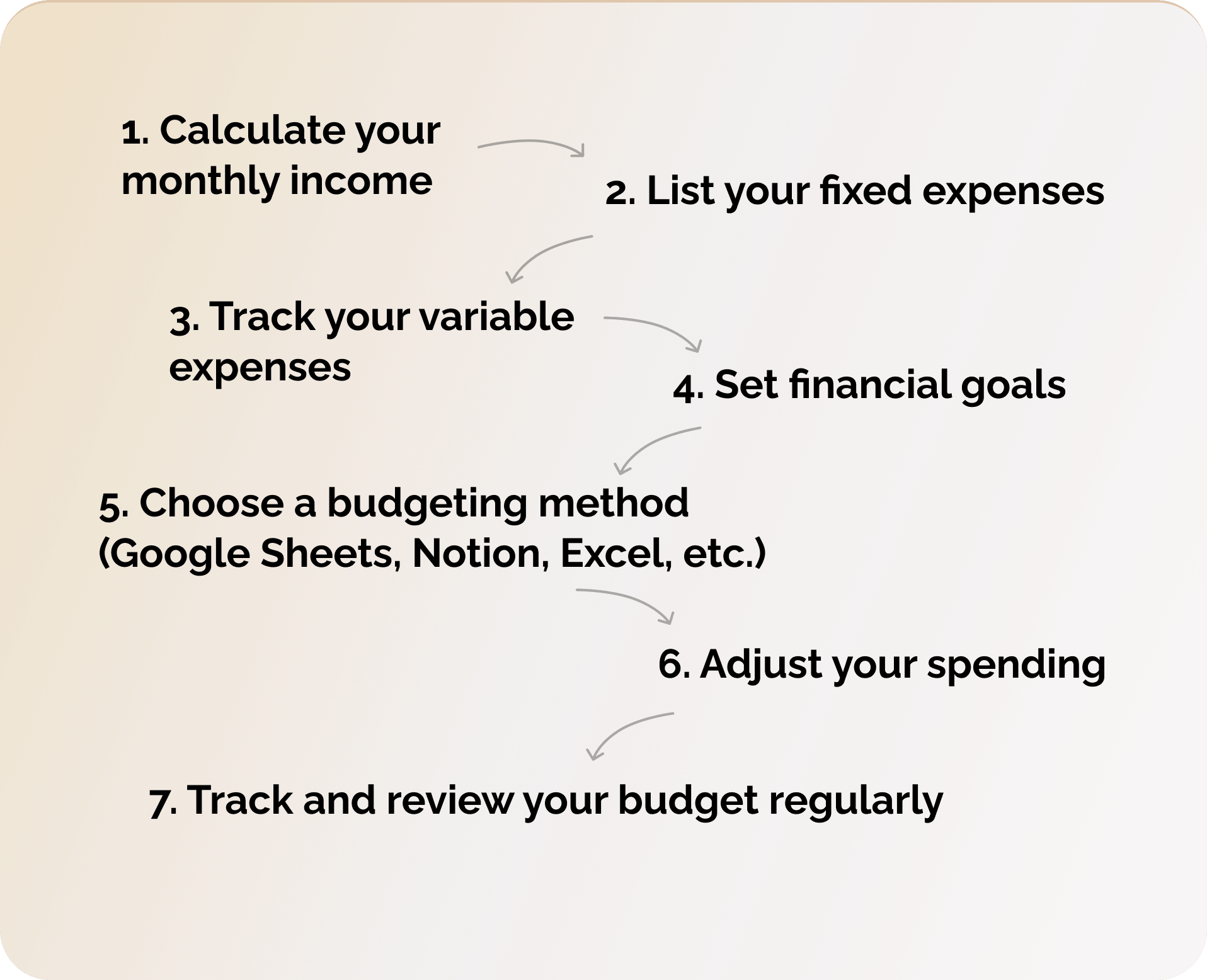

How to make a budget: Step-by-step

Without further ado, here's how to make a budget:

Step 1: Calculate your monthly income

First, figure out how much money you bring in each month. If you have a single source of income, this step will be simple. However, if you have a side hustle or money-producing assets, your income could vary. Tipped workers also have to contend with fluctuating incomes.

If you fall into any of those categories, figure out what your average minimum was over the last 12 months and use that as a starting point. If you make more than that in a particular month, put the money in savings or apply it toward a debt you want to pay off.

Step 2: List your fixed expenses

Next, identify all of your fixed expenses. Don't worry about long-term changes, such as your rent going up when you renew your lease. If a bill will be the same for the next 12 months or more, it goes in the fixed category.

Carefully review your financial records to accurately list all of your fixed expenses. Make sure to include subscriptions, which is something that many people forget.

Step 3: Track your variable expenses

Tracking your variable expenses can be tough, especially when it comes to things like gas and electricity. Don't use your lowest bill of the year as a baseline, as doing so could leave you short at the end of the month. Instead, budget for the average of each expense and adjust as needed.

Your discretionary spending should come last. This includes things like eating out and entertainment.

Step 4: Set financial goals

Once you have a clear picture of how much you have coming in and going out each month, come up with a few goals to work toward. For most people, building an emergency fund is a great first step. If you already have a solid emergency fund, identify debts you want to pay off or a goal you want to save for, such as buying a home.

You can have more than one financial goal at once. Just don't set competing goals, or you'll find yourself frustrated by a lack of progress. For example, you won't be able to pay off a credit card very fast if you're only putting $10 extra toward it every month. If that's one of your goals, put off a different objective until you've achieved that one.

Step 5: Choose a budgeting method (Google Sheets, Notion, Excel, etc.)

There are many great tools out there for building a budget spreadsheet. You can go old-school and create a spreadsheet on Excel or Google Sheets. Alternatively, Notion offers a unique budgeting experience. It allows you to set custom rules, automate calculations, and visualize your cash flow.

If none of these options sound appealing, consider a budgeting app. Our guide to the best budgeting apps of 2026 can help you narrow down your search to a few that are a great fit.

Step 6: Adjust your spending

Here's where the real work comes in. Once you've listed your income and put in all of your bills, you should be able to see where you're overspending. Try to make adjustments so that more of your money is going toward your goals (after your bills are paid, of course).

Most people find that they have room to cut out some excess spending. For you, this could be as simple as making coffee at home or eating out less. Get yourself into the green, then focus on your individual goals.

Step 7: Track and review your budget regularly

You should look over your budget at the end of each week, or any time you make a big purchase. Take time at the end of each month to review your spending as well. Determine whether you stuck to the plan or went off course. If you overspent, commit to getting your budgeting back on track the following month.

Now that you know how to make a budget, let's dig deeper into the different approaches you can try. Remember, the "right" budget for you is the one that helps you achieve your specific goals.

Common budgeting methods

When learning how to make a budget, you'll find that there are different methods to the madness. Here are a few of the most popular approaches.

The 50/30/20 budget rule

If you like percentages, the 50/30/20 rule is a good option. With this system, you divide your income up to put toward expenses in three separate categories:

- 50% for needs, such as housing and groceries

- 30% for wants, such as entertainment, dining, and hobbies

- 20% for savings or debt payments

The 50/30/20 rule is simple, intuitive, and easy to remember. It also encourages you to save or pay off debt, which is always beneficial for your long-term financial health. If things are tight, you can adjust the 30% category and allocate extra money toward essentials or debt repayment.

Zero-based budgeting

The zero-based budgeting method assigns a job to every dollar. Your budget is "zeroed out" at the end of each month. Income minus expenses works out to zero, but not because you blew all of your money. If there's money "left over," you can allocate it toward savings, investments, or paying off debt.

Zero-based budgeting is a great choice for those who want very fine-grained control over their money.

Envelope budgeting

The envelope method is a time-honored approach, but it works. It involves putting cash into envelopes for different spending or saving categories. For example, you might create envelopes for:

- Groceries

- Dining out

- Entertainment

- Gas

Once an envelope is empty, you no longer spend in that category until your next budgeting period. Seeing money "disappear" can help you clamp down. If you don't want to use physical envelopes, there are apps out there with digital alternatives. However, the premise is the same.

Pay-yourself-first budgeting

If you know your income is enough to cover all of your bills and you've got money left over for savings, the pay-yourself-first method could be a good fit. With this strategy, you treat savings as the first "expense" in your budget.

As soon as your paycheck hits your account, put money in savings. Then, pay your essential bills. Anything that's left can go toward discretionary spending. That way, you'll be continually building your savings or retirement account.

Budget categories you should include

You can't learn how to make a budget without including the right expense categories. Here are a few that apply to just about everyone.

Housing

Housing is the biggest monthly expense for most people. This category may include:

- Rent or mortgage payments

- Property taxes

- Utilities

- Home maintenance

- Renters or homeowners insurance

Keeping your housing costs in check will help you maintain a healthy budget.

Transportation

Next up is transportation. Include everything you need to get around, including your car payment, insurance, fuel, and maintenance. Don't forget to plan for surprise vehicle repairs, too. Otherwise, you may have to dip into your savings or take out a loan. Either way, it's a big step backward.

Food and groceries

Food spending usually encompasses both groceries and dining out. Alternatively, you can use this category for all of your food items and anything else you get from the grocery store. Creating a realistic food budget can help you stay within your overall spending plan.

Eating healthy is important, but so is sticking to your budget. Luckily, there are ways to do both. Be disciplined so you can eat foods you enjoy and feel better in the process.

Debt payments

If you carry any debts aside from your house or vehicle payment, list the minimum payments for each. You should also put down any additional payments you want to make, such as credit card balances, student loans, and medical bills.

Don't pay small amounts on all of your debts at once. Instead, pick the lowest one and put extra cash toward it. Once you've paid it off, move on to the next lowest. This is known as the debt snowball method.

Savings and investments

Saving money should always be part of your game plan. Once you've built a healthy emergency plan, put that extra cash toward retirement or investment contributions. If you have to dip into your emergency fund, pause the extra investments until you've rebuilt your primary savings.

Getting out of debt and building a healthy savings account isn't exciting, but it will give you peace of mind when unexpected costs arise — and they will.

Discretionary spending

Discretionary spending includes lifestyle expenses that aren't strictly necessary. Examples include:

- Streaming subscriptions

- Entertainment

- Hobbies

- Travel

- Shopping

When you work these categories into your budget, you can get a better sense of how much you're spending on them and identify places to cut back. After all, do you really need five or six different streaming services at once? Probably not.

Creating specific budgets

Here are some ideas for how to make a budget for specific circumstances and uses:

How to create a family budget

When you're budgeting for the whole family, you'll likely have at least two sources of income. However, you'll also have added expenses, such as childcare, more groceries, and higher rent.

Step one is getting your partner on board. The two of you should sit down and agree on some shared financial goals. Once you're on the same page, you can follow the steps outlined previously to work toward financial freedom.

If you have separate bank accounts, you'll need to be each other's accountability partner. Discuss your spending, review your budget monthly, and look for ways to manage your money more efficiently.

How to create a food budget

Food is one of the easiest spending categories to adjust. It's also one of the easiest to overspend on. Those daily trips to the juice bar or corner store can quickly add up. Don't let them.

Here are a few smart ways to keep your food costs in check:

- Plan a weekly meal menu

- Buy groceries in bulk

- Eat out less

- Save your grocery receipts

After a few months of saving receipts and adding up your totals each trip, you should get better at eliminating waste from your food budget.

Budgeting on a low income

Formulating a budget can be especially stressful if money is tight. Start by prioritizing essential expenses, such as:

- Housing

- Utilities

- Food

- Transportation

You can also take advantage of tools that give you access to short-term cash flow when funds are running low. For example, Grant Cash Advance offers eligible borrowers access to amounts ranging from $25 to $500.

Budgeting for childcare

If you have young children, you may need to cover childcare expenses.

If your kids are already in daycare or after-school care, you should have a relatively consistent bill. If not, consider factors like tuition and meal costs. Some facilities provide lunch, whereas others require you to pack food for your child. You'll also need to consider variables like summer childcare and transportation, which can add up.

Make a point of reviewing your childcare costs regularly. That way, you can be certain that your budget is accurate and reliable.

Conclusion

Now that you know how to make a budget, you're ready to organize your expenses and take control of your financial future. If you find that you're short on money while getting your finances in order, tools like Grant Cash Advance can offer a lifeline. Eligible users can request a cash advance of $25–$500 to fill gaps in their cash flow.

Want built-in budgeting tools to help you save money and visualize where your cash is going each month? As a Grant Cash Advance Plus member, you'll have access to a special Bills & Spending tab. By organizing your income and bills in a user-friendly app, you'll know exactly where every dollar is going.

Sign up for Grant Cash Advance to get the cash you need between paychecks.

Frequently Asked Questions

About the author

Sarah Edwards is passionate about financial literacy and helping readers navigate their money with confidence. She specializes in breaking down complex financial topics into clear, accessible language and regularly covers personal finance, credit, debt, insurance, crypto, and small business. Sarah has contributed to publications such as NerdWallet, MoneyLion, Benzinga, and others.